Where to buy?

Location is a key factor in residential property, so irrespective of the type of property you’re thinking about investing in, it’s worth aiming for the best location you can afford. Look for an area that has strong tenant appeal, offering:

• Proximity to public transport

• Nearby facilities like schools, shops and hospitals

• Lifestyle options including cinemas and restaurants.

Maximising capital growth

With such a diverse property market, rates of capital growth around Australia vary widely. Even within one metropolitan area there can be ‘markets within markets’. Take a look at the checklist below for ideas on how to pick an area with good growth potential:

• Does demand exceed supply?

• Does the area have low prices, which are expected to rise in the near future?

• Are neighbouring suburbs experiencing good capital growth?

• Are there developments happening, or planned for the area, that will have a positive impact on prices?

“The five year average return on property ranges between 15.7% and 25.2% in all capital cities except Sydney, and over ten years, the average return is in double digit figures for every capital city in Australia.”

Noel Dyett, President – Real Estate Institute of Australia, 2008

Which type of property to invest in?

The question of whether to invest in a house, an apartment, a townhouse or a villa may be dictated by price. As Table 2 shows, apartments tend to be more affordable than houses though there can be exceptions to this depending on the condition and quality of the property, its location and the presence of unique features like views. Ultimately it all comes down to thoroughly researching the area you would like you buy in, and matching the type of property with your investment budget.

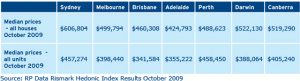

Table 3 Median Values – House or Unit Prices – October 2008

How to buy?

Properties are advertised for sale across a variety of mediums from advertisements in local newspapers through to online agents’ listings. However properties are generally purchased in one of two ways – through private treaty or at auction. Private treaty involves negotiations between a buyer and vendor – often conducted via an estate agent, with a final sale price eventually being agreed on. At this point you will usually be asked to supply a cheque for 10% of the purchase price or a deposit guarantee.

Buying at auction is quite different. The auction tends to be fast and furious with bidding often over in just a few minutes. For investors it is wise to approach an auction with care. It can be easy to get caught up in a bidding war and pay more than you intended. Remember, when you buy at auction the sale is final once the hammer falls. There is no cooling off period – something you may be entitled to with a private treaty sale.

If you’d like to talk to one of our experienced home loan consultants to assess what your investment home loan options are,